Finishes and Interiors Sector (FIS) was invited this week to attend a Round Table hosted by the New Hospitals Programme along with other national trade bodies to understand how we can maximise opportunities presented by programme for members. The discussion introduced the NHP Plan for Implementation as set down by the Rt Hon Wes Streeting MP, Secretary of State for Health and Social Care. The Plan aims to be a thorough, realistic and costed timetable for delivery ensuring the programme is on the soundest possible footing for delivery of our new hospitals. NHP will be backed by up to £15bn of investment for each five-year spending period, averaging £3bn a year by 2030 to be confirmed at regular Spending Reviews.

The discussion focussed on existing supply chain delivery challenges and how this varies regionally, understanding issues such as labour availability, alignment with other major projects and how we can work more collaboratively to support the programme.

Commenting on the meeting, FIS CEO, Iain McIlwee stated:

“This was a good, open and frank discussion and we got into some of the nitty-gritty of procurement, contracting, where and how modern methods construction can be adopted and workforce availability. Ultimately there is a massive opportunity for the sector and it is encouraging that the team at NHP are engaging early and keen to work with the supply chain and help us in addressing some of the challenges.”

More information on the programme is available within the NHP Supplier Guide. FIS has committed to working closely with the NHP and our membership to support the development and delivery of this plan.

The FIS Wage Rate Survey 2025 (data gathered in the first quarter of the year) revealed that, across the trades, FIS members have continued to experience increases in wage rates averaging around 7% in key trade occupations (the full index is available to contributors only).

Commenting on the data FIS CEO Iain McIlwee stated:

“The data underpins that the supply chain continues to be hit by inflationary pressures with an annual increase of 7% in 2025 piling on top of double digit inflation in 2024. If we look at what this means in real terms, for some trade areas rates are now (cumulatively) 75% higher than when we started to gather data in 2020. If we compare this to the wider economy, construction wages continue to outstrip the national average which was below 6% in 2025 and 2025. This is putting real pressure on specialist contractors. Comments gathered as part of the research raised concerns linking this inflation to shortages in key trade areas. If the market does start to improve in 2025 and 2026 there are very real concerns that the skills are simply not going to be there to meet demand. To address this, it is vital that recent Government announcements about investment in skills don’t just get lost in long term strategy, but are invested in supporting employers now in training and developing their workforce.”

The survey also points to changes in the structure of the workforce, which continues to trend away from direct employment, which has fallen from 26% in 2021 to 23% in 2025.

FIS also gathered data on Payment Trends, with around 20% suggesting that payment payment practices have worsened in the past 12 months and less than 5% reporting improvements.

FIS responds to review of the existing national curriculum and statutory assessment system in England. The consultation was launched by the new Government to explore how the the curriculum can evolve to more appropriately balance ambition, excellence, relevance, flexibility and inclusivity for all children and young people.

Specifically it was looking at how the educational system can provide::

an excellent foundation in core subjects of reading, writing and maths

a broader curriculum, with improved access to music, art, sport and drama, as well as vocational subjects

a curriculum that ensures children and young people leave compulsory education ready for life and ready for work

a curriculum that reflects the issues and diversities of our society, ensuring all children and young people are represented

an assessment system that captures:

the strengths of every child and young person

the breadth of the curriculum

In their response FIS raised concerns about the disjointed approach to qualification, the failure to embed a core understanding of careers and key vocational requirements within the existing curriculum.

Two new training courses have been added this week to the FIS e-Learning Hub. The courses aim to support members in managing individual competence associated with key package areas.

The first course is the Firestopping of service penetrations: Best Practice. The aim of this course is to assist in the design, specification and installation of building services penetrations to ensure fire compartmentation is maintained, five leading not-for-profit organisations have been involved in the development of the Guide on which this course is based. The aim of the course is to encourage early consideration of firestopping design in order to avoid problems at a later stage in construction. It is not an installation course but guidance to a good practice approach. The training is broken down to provide information on actions that should be carried out during each of the stages, one to seven, as defined in the RIBA Plan of Work.

The second course is a new interactive Pre-Construction Guide to Drylining. The course has been pulled together from decades of experience and focuses on the lead-up to commencing installation works. It highlights how to check bids and tenders for compliance, understand time requirements and site conditions, and ensure the design information is sufficient and fit for purpose.

Both courses are available freely to FIS members and CPD certificates will be issued on completion.

Speaking on the launch of these courses at the AGM on 7 November, FIS President Ian Strangward said:

“The bank of knowledge which FIS has built is impressive – we now need to make sure that we are not just a font of knowledge, but a modern information provider. It is not good enough to just have information available, we must work smarter to ensure it is used – getting to the right people in the right way. Our e-Learning Hub is going to be key. The first course we put up “an Introduction to the Building Safety Act” has been a great start, several hundred people have already completed the course and feedback has been very positive. In these next courses, “Firestopping of service penetrations: Best Practice” and particularly, our “Pre-construction guide to drylining” you will see progress in the quality of delivery. Now we have a process, you will be seeing a regular flow of new courses targeting vital interventions, job titles and knowledge gaps”

The Fire Wall Labelling campaign launched in 2023 has had a refresh this month with a new web area established to help promote the campaign. The fire wall labelling initiative aims to help identify fire walls and provide instant guidance on what to do when passing cables and pipes through the compartment.

Last year Finishes and Interior Sector (FIS), Association for Specialist Fire Protection (ASFP), and Gypsum Products Development Association (GPDA) joined forces to create this free to use labelling scheme that warns of the dangers of passing cables and pipes through compartment walls (Fire Walls).

The Fire Wall label is a simple and visual way of ensuring that those that could undermine the fire integrity of a wall to realise that it isn’t just a wall, but it is a Fire Wall. The label provides instant guidance via a QR code on what to do when considering whether and how to pass cables and pipes through compartment walls. It runs through a simple STOP, THINK, PLAN, CHECK and RECORD process and provides links to best practice guidance that will help ensure that safety is not undermined.

New requirements in the Building Regulations identify the need for businesses to demonstrate organisational capability. On a basic level, this means businesses will need to evidence how they check people are competent and ensure they are supported by effective process controls that support consistent delivery. This is not really a significant change as businesses have always had a legal requirement to ensure all reasonably foreseeable risks are effectively managed, but it does mean clients and Building Control officers will be showing more interest in your processes and management systems and will have more tools at their disposal to enforce where a business or individual fails to hit the required standards.

To support our community, the FIS Integrated Management Standard (IMS) has been relaunched as part of a newly developed Organisational Capability Toolkit. This toolkit will help members implement tried and proven methods of streamlining their company for the benefit of their business and its stakeholders. The toolkit will help to link and contextualise the wealth of information that FIS members have available to support compliant business management and how they can use their membership to support claims of organisational capability.

This IMS sits as a central resource to help align and control resources. It provides a framework for implementing risk management systems (supported by the FIS Product, Process, People Quality Framework) that will help organisations to meet statutory and legislative requirements.

On relaunching the standard at the FIS Conference and AGM in November, FIS CEO Iain McIlwee stated:

“This standard was developed originally to support the FIS vetting process, but really comes into its own in this new environment. It is clear in our work with members that many construction firms have great processes in place, but there can be a real disjoin between these processes. Across the sector we see design, procurement, contracts and legal, and construction processes that should complement and support each other, however they often clash, cause confusion and conflict and ultimately undermine delivery. This toolkit is a great opportunity to start to look collectively at how we can not just hit the baseline of compliance, but help to raise standards, promote professional businesses and support the Responsible No”.

FIS CEO, Iain McIlwee explores the importance of the word “No” in construction.

The procurement research FIS published in February 2023 coined the expression the “Responsible No”

“No” is a tiny word, one syllable, but at times, the hardest to say. If we say “No” to a clause in a contract, there always seems to be another firm willing to say “Yes”. If we raise too many issues, or qualify too much in our tender response, we may well lose the job. It is easy to talk about “No”, but in a tight, price-sensitive market, with mouths to feed…

The problem is that if we don’t exercise the option of “No”, if we don’t clarify, qualify and draw the line we take responsibility for issues outside of our control, assume responsibility for compliance and sign up to damages and delays that we can’t cover. Even if we avoid the worst of the financial hit, how often do we find ourselves staring at a detail on a construction site, scratching our heads and working it out on the fly – “the site fix”?

Regulation is driving change, common sense demands it

Changes to The Building Act 1984 carried through as part of the Building Safety Act changes, mean that we are liable for that detail for 10 years from a Building Control enforcement perspective and if it impacts fire or structural safety, it could be a 15-year plus liability (with prison sentences if it can be proved we were negligent).

As a sector we pride ourselves on our ability to get the job done, to adapt the design and make it work, but duties in the Building Regulations are now clearer and more onerous. The regulatory environment has changed, a heart full of hope and a tube of mastic isn’t enough.

On higher risk projects we’ve got major and notifiable changes – strict change control processes that should be in place. On all jobs, the building control officer is under greater pressure to ensure evidence is provided – they want to see (or photos of) as-built details backed by evidence of performance and competence.

The principal designer needs to start signing the job off on completion too, it is all about evidence, quality control and information management. If the principal designer won’t support or Building Control won’t sign-off, works stops and with it the flow of monies, I refer you back to the cost of delays mentioned above.

Design liability and elements thereof are being pushed deeper into the supply chain leading to confusion around accountability for design elements. Beyond the intended free-standing additions to the construction contract template, the norm has become to add complex schedules of amendment pertaining to design and programme responsibility. The potential for this to cause confusion around risk and contingent risk, impact insurability and create gaps in insurance cover for specific elements (particularly interface details and fixings) is a real concern. The impact is that businesses, buildings and projects may be uninsured or have significantly less cover than clients currently believe is the case.

Can we fix it?

The old days of “Bob the Builder, can we fix it?” and a rousing chorus of “Yes… we can” is changing. The retort now needs to be more like: “Not necessarily Bob, certainly not until Sarah the supervisor has checked with Alan the architect who has reviewed against the design, clarified with Edna the engineer and Mike the M&E designer, and ensured Quinn the quantity surveyor is aware. We also need to consider if we need to advise Barry the building control officer and he may need to liaise to Bertha the building safety regulator and Ivor the Insurer before … We can!”

This is a cultural change that we need to filter through our supervision protocols, into our Tool Box talks, and embed in our daily processes. But it isn’t just a site thing. Len Bunton always reminds me that dispute resolution begins and most problems could be solved before we sign the contract. There is always risk in construction, but with new potential for delays and new liabilities, we must understand these risks, cap them appropriately and insure them effectively.

Yes, but…

This need for risk awareness is the reason that we have introduced an FIS Contract Review Service. We know that 41% of our members never seek legal advice (scarily only 17% never start on site without a contract in hand!). This subsidised service is about helping members understand the risks and how to push back. It is also about FIS isolating unreasonable requests and pushing back as a collective. Getting your contracts reviewed routinely would be a good New Year’s Resolution. The “Responsible No” is a big ask, but sometimes we do need to say No, it shouldn’t be a flat No, but No, my insurance wouldn’t cover that, No we are not competent to Design that or simply No that is more risk that we can reasonably be expected to take on.

Remember compliance is changing clients have duties along with designers and contractors and good compliant projects supported by a resiliant and professional supply chain are essential. The truth is that we don’t need to say No to everything, but if more of us call out the unreasonable demands, we can start to say Yes to the work, but No to irresponsible asks – maybe we can make 2024 the year of the Confident, well Reasoned “Yes, but…”.

As FIS have explored the competence and capability with our community, the importance of deploying “No” has been repeatedly raised. Ultimately competence and capability require you to know your limits and ensure that all reasonably foreseeable business risks can be effectively managed and addressed.

If we don’t clarify, qualify and draw the line we take responsibility for issues outside of our control, assume responsibility for compliance and sign up to damages and delays that we can’t cover.

The FIS is focussed on Empowering the Responsble No and has launched a campaign to support this.

The Construction Leadership Council (CLC) has published a hard hitting statement calling a halt on the ongoing practice within the construction sector, of industry-approved forms of contract being amended by clients and their solicitors to introduce terms that are onerous and/or difficult to insure. This statement has been issued and is the conclusion to ongoing work through CLC Professional Indemnity Insurance Working Group.

The Construction Leadership Council (CLC), as part of the Building Safety Workstream, established a Working Group to focus on Professional Indemnity Insurance. The key objective of the group was to understand and look to address concerns over the cost, availability and limitations in insurance cover for all parts of the supply chain, from principal designer and contractor through to consultants and specialist contractors. As part this work the PII Taskforce supported an International Underwriting Association event on 31st January 2024 entitled “Competence in the Construction Sector”. The event reviewed new regulatory requirements in the Building Safety Act. Speakers were drawn from the construction, governmental, regulatory, legal and insurance sectors with particular focus on competence requirements and how they may help to reduce risk in the construction process. Wider inference of the Building Safety Act and what can be learned from recent court cases was also covered.

An open panel debate followed looking at the implications on the insurance process. It was recognised within these discussions that, whilst the work on competence is encouraging and should help to reduce risks moving forwards and hence availability of cover. Concerns were raised over design liability being pushed deeper into the supply chain leading to confusion around accountability for design elements. It was noted in discussion that heavily amended contracts add to confusion around risk and contingent risk, impact insurability and potentially create gaps in insurance cover for specific elements (for example, interface details and fixings).

Following exchange between the Insurance Sector and representatives of the CLC confirmed that there is a need to highlight this risk. The key assertion in the statement is that “standard form building and engineering contracts and professional services contracts issued by contract-producing bodies, should be used by clients with no amendments, except where necessary in the context of project-specific risks and relationships. The CLC believes that onerous amendments make contracts unviable, reduce competition, increase risk and lead to unnecessary legal costs required to review legal liabilities created by the amendments”.

Introducing the statement Samantha Peat, Chair of the CLC PII Working Group said:

“A sensible approach will simplify risk allocation, give clarity to the project team and their PII providers, and address the concerns for which the CLC PII Working Group was originally formed, namely, to address concerns about cost and efficacy of Professional Indemnity Insurance in Construction. It will also support the focus on accountability, competence and the need for better information management called for by Dame Judith Hackitt and enshrined within the Building Safety Act and the wider reform of the Building Regulations.”

FIS CEO Iain McIlwee responded:

“This is a massive statement from the Construction Leadership Council – we have to stop this routine amendment of the standard contracts.

This statement echoes the long held concerns of the FIS Community and I would like to personally thank Samantha Peat and colleagues in this Working Group for the amount of time that has gone in to establishing the forum and drawing the right people together to have the open and pragmatic discussion with the insurance industry that has resulted in this clear an unambiguous statement.

We have a legislative process that focusses on duty and a contractual process that focusses on passing the buck – this is bound to create tension. Boundaries need to be reset or we are left with impossible problems, uninsured elements and ultimately the potential for stranded assets and uninsured buildings. T

his is Leadership and we applaud the CLC and supporting representatives from the Insurance Sector for taking a strong line. The statement in itself will not change the world, but what we do with it can. For me the clear message here empowers the Responsible No by starting to spotlight the Irresponsible Ask. Contract amends are at the heart of the cultural concerns in construction – change is inevitable and has I believe been catalysed today”

Through the FIS Responsible No Campaign, the organisation is offering subsidised contract reviews and asking members to report (particularly public sector) contracts that are subject to heavy amends and also provide details of Irresponsible Contractual Clauses so that FIS can address behaviours directly with the client. You can find out more about the FIS Responsible No Campaign here.

FIS has, since it’s outset supported the introduction of the Common Assessment Standard. This new approach was launched in 2019 by Build UK and the Civil Engineering Contractors Association following concerns that the proliferation of suppliers and duplication of effort and support associated with pre-qualification schemes. Through it’s introduction, the claim was that this approach will help the industry to £1bn by eradicating duplicate fees and inefficiencies.

The overall impact, whilst positive (over 22,000 companies now have the accreditation and a growing number of companies have formally adopted use) has not met the ambition and for this reason FIS is adding a Common Assessment call to action to the Responsible No campaign. Underpinning why this is important FIS CEO, Iain McIlwee stated:

“The Responsible No isn’t about digging our heels in, but starting to identify and address behaviours and processes that are barriers to better. This is a clear example of that. The waste here in fees and time is obvious, we have collectively agreed as an industry a better approach and implemented a new standard to do this. We all need to do our bit in helping to raise awareness and normalise this new approach. The reality is we can’t blame people for not doing stuff they may not know about or understand – this is all about helping to identify and explain why something is an Irresponsible Ask.

This is a particularly important time for this intervention with the use of PQQs being linked to new requirements for Organisational Capability enshrined in the Building Regulations and the potential for further proliferation as businesses look for angles to make more money rather than support a collective effort.”

To support this effort, FIS have prepared new guidance on the Common Assessment Standard for members and also a template email to recommend adoption on projects where a particular Pre Qualification scheme is listed as required. Where there is continued resistance to adoption, FIS has also set up a whistleblowing process to enable members to help FIS identify any resistance so that this can be understood and hopefully addressed moving forward.

Finally FIS is asking members to help take stock of where we are now at in terms of impact of the Common Assessment Standard by completing the FIS Pre Qualification Impact Survey here. Information will be used to support this collective effort and to help deliver change.

In a recent residential property tribunal, the roof terrace at Smoke House and Curing House in Hackney Wick, East London was deemed by the tribunal to be a seventh storey bringing it in scope of the definition of a higher-risk building under the Building Safety Act.

The case was brought by a group of leaseholders against the landlord (Monier Road Limited) to ensure remediation work was completed.

The tribunal agreed that Smoke House and Curing House should be classed as higher-risk “for the purposes of Part 4 of the Building Safety Act”:

“In our view, it should be registered with the Building Safety Regulator and have a Principal Accountable person appointed. This is not for the Tribunal to specify under the terms of a Remediation Order, but it is considered essential that this building (both Smoke House and Curing House) are managed under the Higher-risk Building regime. The remedial works should be carried out with an application to the Building Safety Regulator as Local Authorities and Building Control Approvers (previously known as Approved Inspectors) are not permitted to work on Higher-risk buildings.”

It is important to note the Tribunal itself acknowledged it was not within its jurisdiction to formally determine whether the building being considered was a higher-risk building. Until stated otherwise, the sector and regulatory bodies should continue to refer to existing government guidance.

The government announce the introduction of tougher measures to tackle late payments to small businesses.

Secretary of State Minister Jonathan Reynolds has set down his commitment to:

foster a strong payment culture in the UK by bringing the payment performance and behaviour of large companies more clearly into focus.

The Minister confirmed intent to lay secondary legislation “in this parliamentary session” to make it a requirement for large companies to extend information requirements about their payment performance in their Annual Reports. Changes will include the additional requirement to report on value of invoices outstanding and, for construction firms, their practices, policies and performance with respect to retention clauses in any qualifying construction contracts with suppliers. The measures are intended to increase transparency around the payment practices of large businesses and bring them into focus for boards and investors.

The Minister also confirmed that Government will be launching a new supercharged Fair Payment Code to be overseen by the Small Business Commissioner (a voluntary code of best practice for companies committed to fair and fast payments that can be set as a procurement requirement). This will replace the existing Prompt Payment Code, with a clearer and more measurable set of ambitious commitments and will be a further lever to improve the UK’s business payment culture by shining a light on the best performers.

The Department for Business and Trade will also be launching a public consultation “within months” on additional legislative measures to address late payments and long payment terms to ensure improvements in payment times, especially for small businesses and the self-employed.

The Small Business Commissioner, Liz Barclay, said:

I am delighted to announce a new Fair Payment Code will be launched this autumn. The new code will reward businesses that treat their suppliers fairly and pay them quickly. It will also include an ambitious new Gold Award which aims to make 30-day payments the new standard for which businesses can aim.

We need sustainable, resilient businesses at all levels of the supply chains, to achieve the growth the economy needs. That means paying everyone from the largest supplier to the sole trader quicker, so they have the confidence to invest, improve productivity and grow. Fair payment terms and on time payments are the key.

Responding to the announcements FIS CEO, Iain McIlwee said:

The measures on reporting are welcome and mirror the work we supported with the last Government and recently wrote to the Construction Minister (Sarah Jones) to ensure that they did not get lost in the change. The reality is that better measurement will help to isolate the problem, but further consultation and action is required to solve it. We can’t wait for the data to tell us what we already know. The problems the Minister is looking to address are hiding in plain sight.- we only need to look to the spate of recent insolvencies and particularly the devastation caused by the failure of ISG to see the ultimate impact.

We also welcome the changes to the Prompt Payment Code. FIS has worked closely with Liz Barclay and found her to be a powerful advocate for the SME and we will be doing all we can to support Liz in this work and ensuring that the Prompt Payment Code is front and centre on all Public Sector Jobs and principals starts to resonate with Responsible Clients in the private sector too.

FIS will be drawing on the Manifesto already issued to the Construction Minister as the mainstay of our response. Key recommendations included in this document are:

NEAR TERM LEVERS (which have been addressed in above):

More robust enforcement of the duty to report legislation: Improvements to the Payment Practices and Performance (Amendment) Regulations announced in Autumn 2023 are positive, but

need to be backed by effective enforcement. To date there has been no enforcement of the duty to report, and the Prompt Payment Code has not been backed with sufficient resources to deliver the intended changes. The Office of the Small Business Commissioner needs more authority and resource to support effective enforcement.

LONGER TERM LEVERS Reform of the Construction Act is required

The process surrounding application, due dates and pay less notices needs to be simplified to ensure that they cannot be abused. Drawing on international comparisons, the Irish Construction Contracts Act provides for a 30-day payment period from the date at which the payment claim is submitted. This is far simpler than the ‘due date’ referenced in the UK Construction Act, which relies on supplementary information in the contract that can be distorted. There is also less room within the Irish legislation to extend payment terms in a subcontract agreement.

The Construction Act should be amended to ensure retentions are automatically released at the defined date. They should not require additional applications from contractors or relate to dates that are not explicitly related to the completion of their works.

Equally, retention money should be held in trust; it cannot be forgotten that Carillion wiped out £700m of retentions held against the supply chain. Consideration should be given to replicating the recent developments in New Zealand where it has been legislated that retentions are held in trust.

Where Collateral Warranties are held, retentions should be immediately and automatically returned.

The process and cost of adjudication also needs to be considered. Costs will be eased by greater clarity in the Act on payments and better use of standard contracts. Adjudication decisions should be binding to

help avoid costly legal costs/

Make interest on late payment compulsary New EU regulations require compulsory interest payments to be automatically applied to late payment and accrued until payment of the debt. This makes non payment a liability as opposed to an enforcement right that an embattled supply chain is disinclined to impose.

If you have any views on payment reform that you feel should be reflected in FIS Lobbying work, please email iainmcilwee@thefis.org

Conducted in the run up to Fire Door Safety Week, a survey of 2,000 adults found that despite an 18% increase in fires across NHS trusts—averaging nearly four fires daily—52% of people still consider hospitals the safest due to their fire prevention measures.[1]

The survey, conducted as part of this year’s Fire Door Safety Week campaign (organised by the British Woodworking Federation), which runs from 23rd – 27th September, focuses on the theme ‘A False Sense of Safety’. The campaign aims to bridge the gap between perceived safety and actual fire risk, encouraging the public to engage in fire safety awareness and report any fire door issues, regardless of location or the assumption that fire safety is someone else’s responsibility.

When asked about fire safety in other buildings, 36% of respondents considered schools to be as safe as hospitals and 26% felt the same about care homes. This contrasts with recent reports from the East Sussex Fire and Rescue Service where two care home directors were fined nearly £125,000 for multiple fire safety violations, which included defective fire doors and a lack of detection equipment and alarms, across four premises.[2]

Helen Hewitt, CEO of the British Woodworking Federation (BWF) that manages and funds Fire Door Safety Week, said, “Our latest research shows that people often have a greater sense of fire safety in buildings like schools and hospitals. Regardless of where you are, it is crucial to be aware of fire safety measures, such as emergency exits and fire doors, because the risk of fire is present in any building.”

When considering building safety, emergency exits were cited as the most important factor in feeling safe by 75% of respondents, followed closely by visible fire safety measures, including alarms and fire doors (70%). Additionally, 46% of respondents said they always or often notice fire doors in the buildings they visit. Regarding the buildings where respondents believed fire doors are well-maintained, 47% felt that fire doors in public buildings, such as hospitals and cafes, are properly maintained.

The survey also found that 29% of people would not report a fire door issue because they would not know who to contact, despite 74% saying they would report a door that appeared damaged. Concerningly, this is a decline from last year’s campaign, ‘Recognise it, Report it’, where 86% said they would report a faulty or propped-open fire door. For unresolved fire safety concerns, 43% would escalate the issue to the Health and Safety Executive, while 5% would not escalate it at all, and 14% did not know who they would escalate it to.

Helen added, “Fire doors are crucial in preventing the spread of fire and smoke. It’s encouraging that more people are noticing fire doors in the buildings they visit, but there’s still work to be done to ensure people feel confident in spotting and reporting fire door issues. Knowing who to report these problems to is key—start with the premises manager or owner, and escalate unresolved issues as needed. With the correct information, we can all contribute to maintaining fire safety.”

Fire doors require expert maintenance to remain effective. However, 29% of respondents would trust management and 27% would trust the building owner to handle fire door issues, while 13% would trust a handyman and 19% a caretaker. For fire doors to function correctly, they must be installed and maintained by a competent, trained professional.

Gavin Tomlinson, Protection and Business Safety Scrutiny Committee Chair of the National Fire Chiefs Council (NFCC), said: “Fire doors are an essential feature in most buildings, helping to protect both occupants and responding firefighters in the event of a fire. When well-fitted and properly maintained, fire doors provide vital protection against the spread of fire within buildings. While legislation requires those responsible for fire safety to have arrangements for testing and maintaining fire safety measures, people should feel safe in the buildings they visit or work in, and they should feel empowered to report faults and raise concerns, particularly those related to fire doors.”

Discussing the ongoing importance of Fire Door Safety Week, Helen Hewitt commented: “This campaign raises awareness of the critical role fire doors play in saving lives. The support we receive each year from individuals and businesses helps us spread this important message.”

For more information and an amazing set of fire door safety resources visit:

www.firedoorsafetyweek.co.uk

On Fire Door Safety Week 2024, FIS launched the Walls as a System document which has been developed by a collaboration of trade bodies and technical experts and looks at the design and build of wall systems, including integration of doors. To download a copy of the guide click here.

The government has, this week, unveiled new measures to support small businesses and the self-employed by tackling “the scourge of late payments”. New legislation being brought in the coming weeks will require all large businesses to include payment reporting in their annual reports – putting the onus on them to provide clarity in their annual reports about how they treat small firms. This will mean company boards and international investors will be able to see how firms are operating. Enforcement will also be stepped up on the existing late payment performance reporting regulations which require large companies to report their payment performance twice yearly.

The announcement by Business Secretary John Reynolds also sets down an intention to consult on tough new laws which will hold larger firms to account and get cash flowing back into businesses – this is seen as key to supporting growth.

How are requirements changing?

Under current laws, responsible directors at non-compliant companies who don’t report their payment practices could face criminal prosecutions including potentially unlimited fines and criminal records.

A new Fair Payment Code will replace the old Prompt Payment Code, and will be open to signatories this autumn. Businesses will need to prove they have met good payment standards before being awarded official code status.

This will be designed to push businesses to pay faster more often, to be awarded either gold, silver or bronze status. The Code will also shine a light on those responsible businesses doing the right thing by their suppliers and small firms.

It comes as part of our wider work to support SMEs to help go for growth with reform to business rates, getting more small firms exporting and our new industrial strategy.

A consultation which will be launched in the coming months, which will also consider a range of further policy measures that could help address poor payment practices. These new proposals, subject to consultation, will be bought forward on audit and audit committees, in order to help rebuild small businesses’ trust that they will be paid on time and to deliver on Labour’s manifesto commitment to tackle late payments.

Prime Minister Keir Starmer said:

We’re determined to back small businesses by unlocking their barriers to growth, and stamping out late payments is at the heart of this.

We know how important it is for business owners to have the peace of mind and certainty around their cashflow to keep their businesses alive. Late payments cost businesses tens of thousands of pounds and is one of the biggest reasons businesses collapse.

After years of delay, we’re bringing forward measures that small businesses have long been calling for to tackle late payments once and for all.

Business Secretary Jonathan Reynolds said:

Late payments are simply unacceptable and this government is determined to level the playing field for small business. When the cashflow runs dry, small firms go under which is why we need to hold larger business to account with their payment practices and foster an environment that supports growth and jobs.

Slashing trade barriers, reforming business rates, getting more SMEs exporting – this government is committed to small firms. We know there’s a lot more to be done, but today we are calling time on late payers once and for all.

New research published by the Department for Business and Trade has found payment problems multiply the further down the supply chain you go. With delays to payments increasing with each business along a supply chain, this results in smaller businesses generally experiencing more issues with late invoices than larger firms.

These new findings underpin the need to move quickly to crack down on late payments. The research also found that there was a clear imbalance between big and small firms, and that administrative errors are a major factor in creating slow payments with 24% of firms saying that invoices being incorrectly handled added to delays.

The government will work closely with industry to discuss what further measures can be considered to crack down on late payments while ensuring we strike the right balance and avoid excessive burdens on businesses.

The Small Business Commissioner, Liz Barclay, said:

I am delighted to announce a new Fair Payment Code will be launched this autumn. The new code will reward businesses that treat their suppliers fairly and pay them quickly. It will also include an ambitious new Gold Award which aims to make 30-day payments the new standard for which businesses can aim.

We need sustainable, resilient businesses at all levels of the supply chains, to achieve the growth the economy needs. That means paying everyone from the largest supplier to the sole trader quicker, so they have the confidence to invest, improve productivity and grow. Fair payment terms and on time payments are the key.

FIS Reaction

FIS has welcomed the announcements. The organisation had already been in touch to express concern that legislation due to be laid before Parliament before the snap election was called in June had been delayed. In their letter to Construcion Minister Sarah JOnes MP, FIS made the following statement:

<in construction> Large firms help enable projects, but it is the supply chain of SMEs who will need to find and invest in the 66% growth in the workforce we will need to deliver the homes that Labour is expecting. These SMEs find themselves at the mercy of inept and at times immoral procurement practices, contractual processes that leave them picking up the full risk of mistakes and omissions by others and credit and payment terms that make it almost impossible to plan and invest effectively as businesses.

SMEs are constantly paid late with appalling credit terms that often see them exposed to 90 days + of cost on a job before they receive a penny. With little protection available from insurance, this is offset by trade and charge card credit on materials. These SMEs have no protection from upstream failure and a raft of these in recent months has rocked our supply chain. Tracking payment practices (value not volume) is not enough (we need to look at how the supply chain is protected with bonds and project bank accounts), but a worsening payment trend can give the supply chain vital warning of a looming failure.”.

In her response, the Minister provided some reassurance that the new Government do understand the severity of the situation.

The Government is committed to creating a better business environment for small businesses. This includes taking action on late payments, to ensure small businesses and the self-employed are paid on time, and to increase transparency in relation to payment performance. Whilst the draft Statutory Instrument introduced earlier this year had to be withdrawn, the Government is fully aware of the importance of these changes to the payment reporting requirements to subcontractors in the construction sector. Therefore, it intends to reintroduce this legislation at the earliest opportunity. The legislation is now expected to be re-laid before Parliament in 2024, enabling commencement in 2025.

You can see a full copy of the Minister’s letter (in which she also expresses gratitude for the proposals set down in FIS Manifesto) here here.

Following the recent unfolding situation with ISG, FIS Associate Member and insolvency practitioner BABR has clarified what this means for affected businesses and provide guidance on what you should do next.

Understanding Administration Administration is when a company is given legal protection from creditors while an appointed administrator attempts to rescue the business or achieve a better outcome for creditors than liquidation would provide. During this time, creditors generally cannot pursue claims against the company without court permission.

It’s important to note that in cases like this, immediate payments to creditors are rare, except in exceptional circumstances. Most creditors will need to wait for the administration process to be completed, which can take time. Therefore, it’s crucial to manage expectations regarding cash flow.

Likely next steps for affected members:

Monitor developments: Monitor announcements regarding ISG’s situation closely. The outcome of administration could range from a restructuring and continuing business to liquidation.

Review your position: Now is the time to carefully review your contracts, outstanding payments, and ongoing ISG projects. Since payments are likely to be delayed, you may need to adjust your cash flow planning accordingly.

Prepare for delays: Be prepared for a lengthy process. The administration process can be slow, and in many cases, creditors receive only a fraction of what they are owed, if anything at all.

How to manage cash flow:

Cash flow solutions: Given the likely delays, consider short-term financing or invoice financing to maintain liquidity.

Renegotiations: Speak to other clients and suppliers to potentially renegotiate payment terms or request upfront payments to help cover any cash flow gaps.

Seek professional advice: It may be beneficial to consult professionals such as insolvency practitioners, accountants, or legal advisers specialising in business restructuring and financial distress. They can guide your situation, help you explore your options, and protect your business.

We understand that these developments may cause concern, and we’re here to help support you through this period of uncertainty.

If you have any specific queries or require assistance with any financial issues related to ISG, please don’t hesitate to contact BABR directly on its dedicated helpline number, 03332 419 014, exclusively available to FIS Members.

To find out about BABR support available to FIS Members click here.

Following confirmation that ISG Group and all subsidiaries are entering administration the Construction Leadership Council Convened a meeting and has published the following statement

“This morning, the Construction Leadership Council convened a meeting between key construction trade bodies, education and skills providers and the Department for Business and Trade to discuss how industry should respond to ISG filing a notice to enter administration.

Our sympathies are with everyone across the industry who is directly or indirectly affected by the administration of ISG, and the CLC’s objective is to ensure that individuals and organisations impacted are given the appropriate support and guidance, and that as far as possible the effect on the wider sector is limited.

The CLC is collating detailed guidance available for those impacted and in the interim, we would advise everyone in the industry to ensure that they are managing any impact on their businesses within the terms of existing contracts, ensure that where possible payments are made promptly to suppliers and to await further information. If companies are in particular financial distress, we would encourage them to contact their relevant industry body.”

For the apprentices and graduates who are directly employed by ISG, Build UK and the CITB have established a working group to ensure that placements can be found for as many people as possible. If you or someone you know is an apprentice or graduate directly employed by ISG, please contact info@builduk.org in the first instance.

FIS will circulate this guidance as soon as it is available, but in the meantime, we refer members to the key points from our update on Thursday:

When you are able to access site (do adhere to timings provided) recover any plant, site accommodation and any records that are currently on the sites. You should avoid at all costs any damage to your completed works.

if you are able, take photographic, video and written records of your work in progress.

Accurate and detailed records will be invaluable in establishing the value of your “final account” and can be used for any negotiations with main contractor who is brought in to complete the contract.

You should prepare a schedule that shows a record of all outstanding payments including retentions and when these payments were due

If you’re currently in possession of materials that are required for the contract but have not been delivered to the site then make careful note of these.

FIS contract and legal advisors are on hand to help and some have offered additional pro bono support to members to help review contracts to ensure you are clear on your contractual position with respect to an administration event and e.g. understand Step in Rights from clients. If you need advice please send your contracts to iainmcilwee@thefis.org and we will look to undertake a targeted contract review.

We have had a number of questions with respect to Project Bank Accounts, these should protect and ringfence any monies due – certified payments should progress. Any applications will need to be certified and could be subject to a delay. Clients will be looking to appoint a contractor to replace ISG. How they are able to progress the project and the impact on existing sub contractors will depend on the contract and funding. We will be working with CLC and pressing clients to manage transition with sensitivity to the impact on the incumbent suppliers.

Members impacted are advised to do a cash forecast and, if the situation with ISG is forecast to cause serious financial difficulties, then we have specialist advisors available to assist you and provide guidance.

We would also ask members to send us in confidence details of the contract they are working on, size of the contract and monies owed (certified, a valuation of any completed works currently uncertified and retention).

FIS is aware of the unfolding situation with respect to ISG. As of today, our understanding is that ISG Construction Limited, ISG Engineering Services Limited, ISG Retail Limited, ISG Jackson Limited and ISG Central Services Limited have filed for administration.

It is important to note that ISG Fitout Limited(which accounts for around £500m and was profitable at the point of last filing) has not been included in the application. The parent company, ISG Limited, has, so far, not applied to the court. At this stage we do not have clarity on how these parts of the business will be impacted and you are advised to stay in close contact with your nominated contact if you are currently in contract.

Clearly this is an unsettling time for the supply chain and ISG staff members. FIS will be doing all we can to advise and support all involved.

If businesses are currently engaged by or are about to start work for any part of the ISG Group that has filed for administration, these contracts will be automatically terminated. FIS Commercial Advisers have indicated that it is highly likely that all affected ISG sites will be shut immediately. Any claim will be managed by the appointed administrator in due course. It is suggested that you still attend at your sites and recover any plant, site accommodation and any records that are currently on the sites.

If you are able to access site, then it is important that you take photographic, video and written records of your work in progress. These records will be invaluable in establishing the value of your “final account” and can be used for any negotiations with any main contractor who is brought in to complete the contract. You should prepare a schedule that shows a record of all outstanding payments including retentions and when these payments were due, if they are unpaid. If you’re currently in possession of materials that are required for the contract but have not been delivered to the site then make careful note of these and further advice will be provided in due course as matters unfold. You should avoid at all costs any damage to your completed works.

It will be helpful if you could send any information regarding the status of projects to FIS. In order to ensure we can provide the best possible advice and support, please forward any communications that you receive from the employer, the design team and also the Administrator in due course.

FIS and our advisors will do all we can to support members and we will be working with colleagues from across construction, Government and stakeholder groups to provide a united response in what is a very difficult time.

Our helpline can be accessed via 0121 707 0077 or you can Email: iainmcilwee@thefis.org with any questions or concerns that you have.

Apprentice and trainees who have been employed by ISG and are looking to source alternative employment should register their details with BuildUK who are co-ordinating this aspect of the industry response and please contact info@BuildUk.org. Other members of the team or employers in the sector who can offer alternative positions for trainees or employers, please email iainmcilwee@thefis.org.

FIS Project Reuse is live and underway. Encouraging reuse was highlighted as a priority for the FIS Sustainability Leadership Group. Following several round tables and working group discussions FIS has decided to take the plunge and set up a pilot storage facility in East London. This facility will help us to isolate and resolve the issues that are blocking a more systemic approach to re-use in key product areas. The pilot will interrogate barriers, potential commercial models and start to create a end-to end process supported by appropriate standards that will help to normalise and industrialise re-use.

The pilot will focus initially on suspended metal ceiling tiles and luminaires. The project is viable thanks to the support and financial contributions of 10 amazing pioneer partners from all parts of the supply chain. This intrepid group drawn from architects, fit-out contractors, strip out contractors, sustainability consultancies and manufacturers bring deep knowledge and a great balance of outstanding skills and practical experience to the table.

As a first step we have identified some ceiling tiles which will, hopefully, make their way to the storage facility shortly and we are visiting the site where they are currently installed next week. This process will help us understand what information is required to ensure that the process of finding a new home goes as smoothly as possible.

This project has the potential to create the framework to develop a universal marketplace for reuse products and thereby reduce waste and the carbon impact associated with fit-out projects.

We need your support to make sure we can take the project to the next step and continue on the great work that has been started. Contributions range from £2k to £5k. If you want to know more about or be part of a great project, please contact me at flavielowres@thefis.org

To find out more about the project and see our list of amazing pioneer partners click here

FIS today congratulated the new UK Prime Minister Sir Kier Starmer and his colleagues on their election success as Labour forms the new Government.

FIS CEO Iain McIlwee noted that “A new Dawn for the UK, means it is essential to deliver a new Dawn for Construction. The UK Construction Industry is at the beating heart of the country, enabling all other parts of the society and the economy to function and succeed. The construction sector is worth 9% of GDP to the and employs over 2.5 million people. But it is more than that, it provides our homes and infrastructure, it shapes our cities, preserves our heritage, provides our shelter and shapes our lives – great buildings are at the heart of a great nation.”

Two key areas of important focus for the new Government in their hundred day plan are:

Firstly Government as a procurer has perennially missed the opportunity to harness the potential of construction to support socio-economic development. Best value procurement is delivered by following principles of the Construction Playbook, but the Playbook is routinely ignored. Investment in the Value Toolkit took this a stage further, but this has never been realised. Section 106 and equivalent procurement interventions needs an urgent rethink to align to the Playbook and ensure value outcomes are measured on a National Level – more devolution is coming, but it should enhance not replace a national strategy.

The reality of building more homes (more anything) is we need more people. We have spent a generation building an industry around immigration, so this reform is going to take time and the infrastructure is not there (in our sector we need to double the best we did since 1974 to maintain the workforce we need).

Government needs to stop quoting International Benchmarks about arbitrary educational levels and “future skills” and look at what we need now. The landscape for L2 and L3 Apprenticeships has been decimated. The average apprentice is now over 25 and studying for a higher or advanced level apprenticeship. Only one in five apprenticeships is in a shortage occupation.

We need 1 in 10 people to choose to work in construction and we need them more work ready than they are now. The role of the education system is to get people work ready and it then becomes the responsibility of the employer to turn work ready to competent and develop them. Our reality is that kids leave school (and often college) nowhere near work ready and conditioned to think of construction as a last resort, not recognising we are the bedrock of all social and economic evolution. The dialogue in schools about our industry needs to change, it is a well paid and essential sector. This was evidenced in the chaos of Covid when Government failed to deem construction essential workers, but still needed the “essential work” done.

In the meantime, we need an approach to migration and the Shortage Occupation list to be an agile stop gap solution.

We also caution Labour to consider carefully their plan to be tough on contingent workers. Government needs to be mindful of a quote that jumps out for me from the Reading Report:

“To invest in a directly employed workforce would render many firms uncompetitive given the limited focus on genuine and enduring collaborative relationships that procurement practices allow. The consequential reliance on contingent forms of labour is an issue of commercial reality rather than preference but has a detrimental impact on the training culture.”

Finally the Building Safety Act is a force for good, but there are some big gaps. A key to tightening is to ensure that a Design Responsibility Matrix in included in the list of regulated documents for the Building Safety Act, ensuring that this vital mechanism to make system based decisions based on the right advice at the right time is in place.

A new stricter procurement regime is being introduced to support the Government’s 2019 Manifesto commitment to ‘..support start-ups and small businesses via government procurement, and commit to paying them on time…. <and> clamp down on late payment more broadly…’.

The Public Procurement Notice PPN 10/23 comes into force on the 1st April and demands historic payment performance is taken into account when awarding new Central Government contracts with a value in excess of £5 million per annum.

Contracting authorities must verify that the successful bidder meets the selection criterion prior to award of the contract or appointment to a framework agreement or dynamic purchasing system. The criterion is based on:

Whether the bidder has paid its suppliers in accordance with the contractual terms that it applies to its supply chain; and

Whether, overall, the bidder has paid its suppliers promptly by:

paying at least 95% (at least 90% if an action plan is provided) of invoices within 60 days, which is considered an appropriate measure of overall payment promptness, and;

meeting the average payment days threshold of at least 55 days for all invoices.

Reporting on this requirement will take into account a twelve month period and the bidder must demonstrate that they meet the required standard in at least one of the two previous six month periods – intercompany payments should not be included.

Where the bidder has reported payment data every six months in accordance with the Reporting on Payment Practices and Performance Regulations 2017, the two most recent reports can be submitted. If the bidder has recent data for the previous three or more months which has not yet been reported under the regulations, then this can also be submitted as a reporting period.

The criteria for applying the rules is summarised as:

Bidder pays ≥95% of all supply chain invoices in 60 days and the bidders average payment days are also ≤55.

Both metrics are hit concurrently in at least one of the previous two six month reporting periods.

Bidder meets the required standard.

Pass

Bidder pays ≥90% < 95% of all supply chain invoices in 60 days and the bidder’s average payment days are also ≤55.

Both metrics are hit concurrently in at least one of the previous two six month reporting periods.

Bidder demonstrates action plan that includes (as a minimum) the following: 1. Identification of the primary causes of failure to pay: (a.) 95% of all supply chain invoices within 60 days; and (b) (if relevant) all supply chain invoices within agreed terms. 2. Actions to address each of these causes. 3. Regular reporting on progress to the bidder’s audit committee (or equivalent). 4. Plan signed off by a director. 5. Plan published on its website. (This can be a shorter, summary plan)

Pass

Bidder pays ≥90% < 95% of all supply chain invoices in 60 days and the bidder’s average payment days are also ≤55.

Both metrics are hit concurrently in at least one of the previous two six month reporting periods.

No action plan or action plan does not include all of the above features.

Fail

Bidder pays <90% of all supply chain invoices in 60 days in both of the previous six month reporting periods after removing intercompany payments (if relevant).

Bidder’s payment performance falls substantially below the required standard.

Fail

Bidder’s average payment days are >55 in both of the previous six month reporting periods after removing intercompany payments (if relevant).

Exemptions should only be considered:

where the market for a contract of this type is distorted/narrowed/struggling to such a significant extent that delivery of public services is likely put at risk, or value for money is likely to be severely compromised;

where there is a civil emergency.

FIS CEO Iain McIlwee commented:

“Whilst this another positive step, we are still talking about lengthy payment periods in an industry where up-front costs have increased substantially in recent years. It is also narrow in application, the requirement to comply with this notice only binds Central Government Departments, their Executive Agencies and Non Departmental Public Bodies where the contract value exceeds £5 million. It does not apply to NHS trusts, local or devolved authorities and there is also a fair bit of wiggle room provided in the exemptions. All this means in real terms the impact will limited for the vast majority of those working in the finishes and interiors sector. That said it is further recognition of the importance of an issue which remains a cancer at the core of construction and our hope is that as procuring authorities look to the new Regulatory Requirements and concerns about the resilience of the supply chain that they look to exceed the expectation set down in this PPN.

With increased Government support it is more important than ever that we call-out poor practice. If you have payment concerns FIS is able to take these foward anonymously both directly and working with the Small Business Commission (who has sanctions via the Prompt Payment Code). Through FIS you also have access to QS, Legal and specialist credit checking services that can help to expedite payment – nothing changes if we do or say nothing and we will always look to act in your best interests”.

The FIS Wage Rate Survey H2 2023 conducted in January 2024 revealed that, across the trades, FIS members have continued to experience wage rate increases averaging around 4% in key trade occupations (the full index is available to contributors only.

The survey also explored some of the concerns that are currently being experienced related to risk dumping through the supply chain.

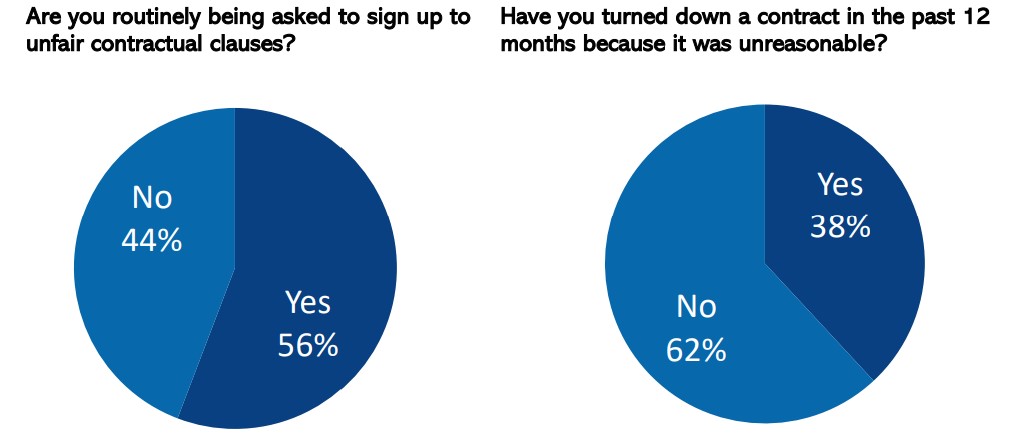

Commenting on the data FIS CEO Iain McIlwee stated:

“The numbers clearly shows that the supply chain continues to be hit by inflationary pressures. Some of the contractual issues are also a worry, close to 60% of our specialist members are being asked to sign unfair contracts. Encouragingly there is evidence here that the Responsible No is being exercised, but the numbers are still out of balance. There is also evidence that design, programme and compliance risk are increased with over 70% stating that they routinely being asked to take more risk in terms of Design and close to 90% stating the same for programme. These numbers are not surprising, but they are concerning, especially against the backdrop of rising cost and more limited insurance cover available“.

In 2024 FIS launched the Responsible No Campaign to help bring attention to the pressures that specialists are under and the indiscriminate risk dumping that is evident in parts of the supply chain.

IF you wish to participate in future wage rate surveys, please contact the FIS on info@thefis.org and we will make sure you recieve appropriate updates.