Whilst uncertainty has dominated headlines, workloads in the finishes and interiors sector held up well in the quarter. The picture is more mixed when we look to sales, with the balance experiencing growth reducing from 29% to 17% (when comparing to the last survey period) and those experiencing a decline increasing from a fifth to a third of respondents.

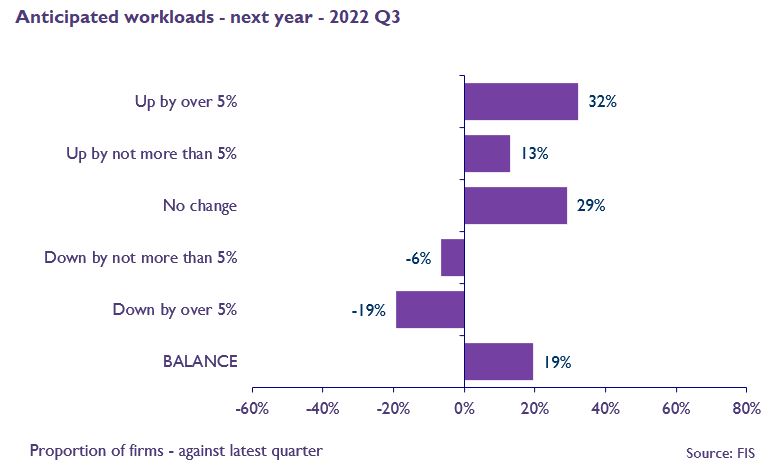

Against a backdrop of uncertanty, looking ahead to 2023, those predicting growth in sales are in the minority (just a fifth of responses). Those seeing the market as static or declining are equally split leaving an overall balance of 20% anticipating a reduction in sales. Again the picture for workload is more optimistic with sales from 2022 washing through and a balance of 19% still anticipating growth. Concerns were experessed about the sub-contractor squeeze as tender price increases do not fully reflect the significant increase in operating costs.

Uncertainty is casting doubt on the viability of some future projects with nervousness amongst investors linked to political and economic uncertainty. It is therefore not surprising to see demand move ahead of labour shortages as the biggest expected constraint for the marke, however, commentry still flags the “alarming lack of quality and reliable labour”.

The full FIS State of Trade Survey Q3 2022 can be downloaded here.