CLC Latest: Material Supply Chain Group

Statement from John Newcomb, CEO of the Builders Merchants Federation and Peter Caplehorn, CEO of the Construction Products Association, co-chairs of the Construction Leadership Council’s Material Supply Chain Group.

As the first quarter of 2024 draws to a close the latest report from Construction Leadership Council’s Material Supply Chain Group (formerly Product Availability Group) continues to show good levels of product availability across the board.

The beginning of 2024 has also brought early signs of improvement in construction activity, although housebuilding is expected to be flat for most of the year.

Overall construction activity trended upward in January and February reaching its highest level since August 2023, despite poor weather. The weather is likely to have affected sales volumes through builders’ merchants, which remained static during the first two months of the year. Most regions, however, saw an increase in volumes in March and there are hints of pent-up demand as a handful of regions are showing high levels of sales compared to 2023.

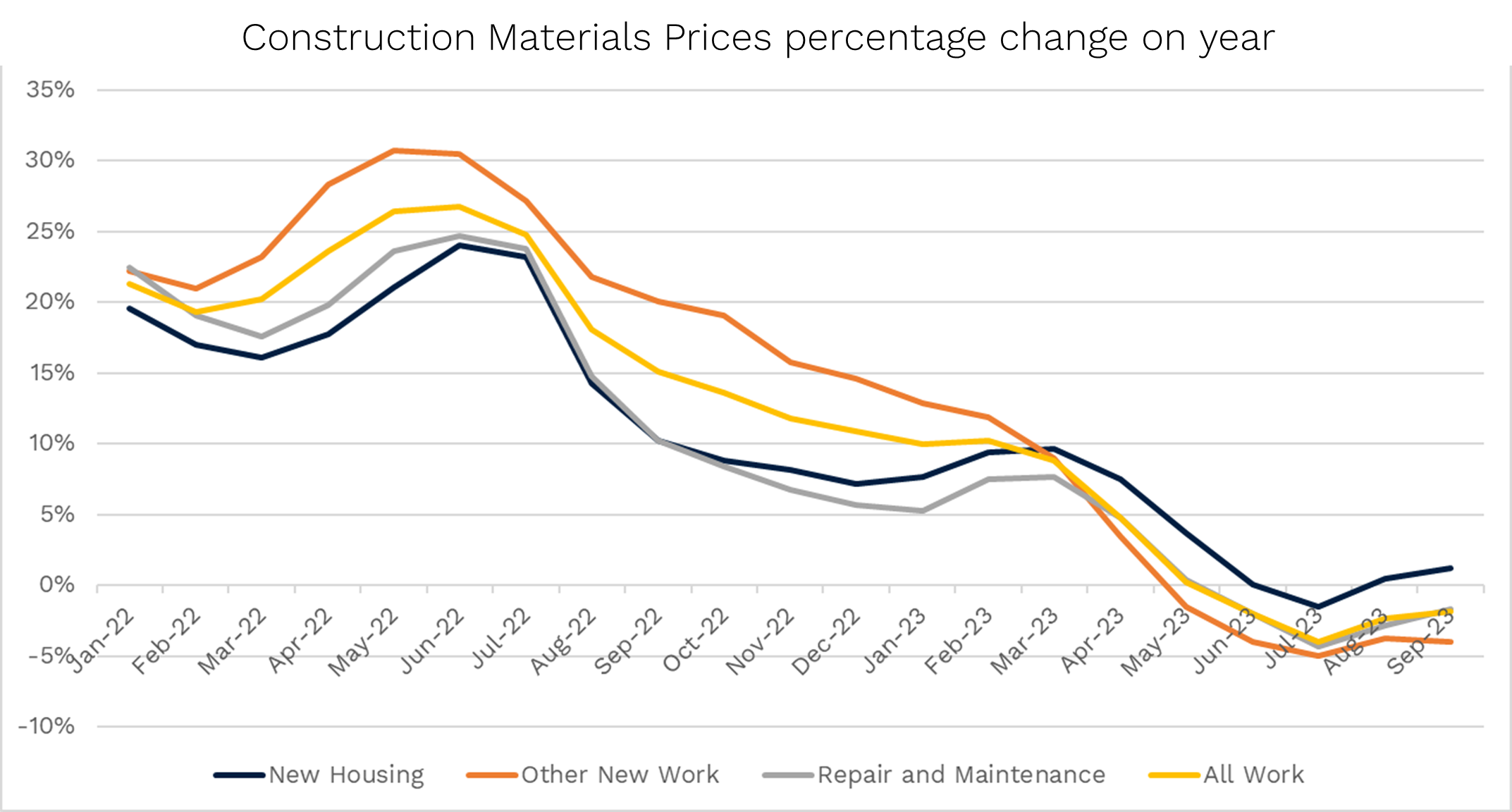

Prices generally have increased by 3 to 4%, which mirrors the wider economy where CPI inflation in January was 4.0%.

Previous concerns about the impact on products normally transported via the Red Sea seem to have dissipated or are manageable. Although some are experiencing increased shipping costs and slight delays in delivery of ironmongery and sanitaryware this is now described as an ‘inconvenience’, and not a major issue.

Separately, the electro-technical sector has flagged concerns about the ongoing geopolitical risks in East Asia and the potential impact on any construction products, plant and tools with chips sourced from that region. The Group is considering adding this issue to its ‘horizon scanning’ and some members are independently analysing the situation.

However, the availability of skilled labour (outlined in the Group’s report of 20 February 2024) remains the most immediate and pressing concern for most in the Group, with several expressing the view that current market conditions have been masking the true scale of this issue, which will be exposed when the market picks up. The Group has shared these concerns with the CLC’s People & Skills Group where they will be taken up in further detail.