CPA Trade Survey reports another mixed quarter for the construction supply chain

The CPA’s latest Construction Trade Survey for 2023 Q2 showed a mixed view on activity across the construction supply chain. Here are some key findings from the latest survey:

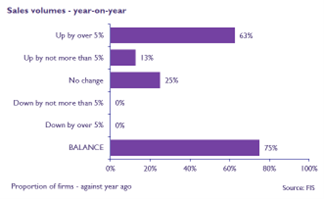

Output & Sales: A mixed quarter for product sales, workloads growth for SME contractors and chartered surveyors was split by sector of activity.

Expectations: Manufacturers’ expectations were mixed, new orders increased for civil engineering contractors, SME enquiries increased overall, but growth was driven by a sole sector.

Costs and Constraints: Costs moderated in Q2 but inflation remained broad-based, with issues related to finance and labour availability rising in prominence.

FIS Members - access your copy now

Read the full results from surveys across the construction supply chain by clicking the button below.