by Clair Mooney | 7 Mar, 2023 | Contractual and Legal, Lens Blog, Main News Feed

FIS Consultant Len Bunton looks at the importance of keeping records and why this is vital. It is not uncommon for disputes to emerge on contracts that were concluded 3-4 years ago, so your records need to be collated and stored and archived, because you never know when you might need them.

These monthly Blogs are designed to help FIS Members avoid common traps and build on our focus on collective experience. They share ideas about improving the commercial management of your contracts. In other words, instilling best practice into the way FIS members run and manage their business. What I have endeavored to suggest is ways to ensure you get paid on time, and what you are due.

by Clair Mooney | 1 Mar, 2023 | Main News Feed

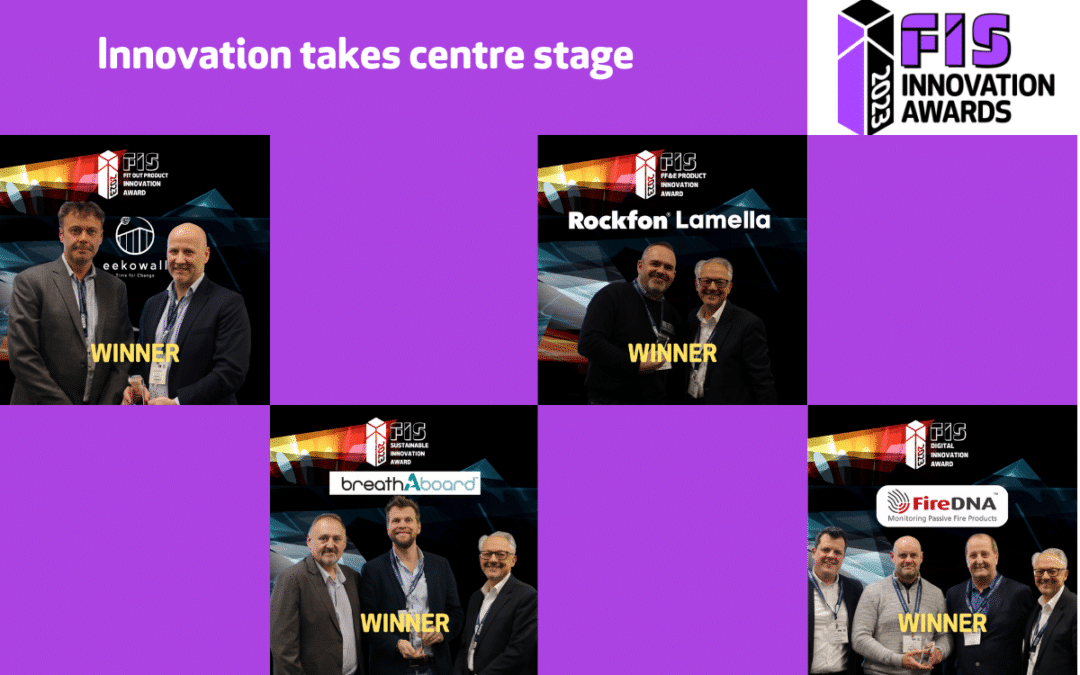

FIS announced the winners of its inaugural Innovation Awards at a ceremony held at is Conference in London.

In front of a packed audience at the Business Design Centre, the winners of the 2023 FIS Innovation Awards were announced and presented. The Awards recognise and celebrate innovation in the finishes and interiors sector showcasing companies that are paving the way for greater efficiency and collaboration. The aawards comprised four categories: Product Fit-Out, Product FF&E, Digital and Sustainability.

All entries were independently assessed by a panel of expert judges and the winner of each category was announced in front of a live audience. The winner of each category was then invited to deliver a short pitch on their innovation to the audience, who then determined the overall 2023 Innovation of the Year winner.

The 2023 award winners are:

Innovation of the Year

FireDNA for its Passive Fire Product Monitoring Software

Product – Fit Out

Eekowall for its off-site manufactured eekowall panels]

Product – FF&E

Rockfon for its modular slatted wood acoustic wall system, Lamella

Sustainability

Adaptavate for its plasterboard alternative, Breathaboard

The awards and event were supported by sponsors Etag Fixings, Protektor, Fire DNA and Payapps.

by Clair Mooney | 27 Feb, 2023 | Main News Feed

The University of Reading, Finishes and Interiors Sector (FIS) and AMA Research (part of Barbour ABI) have today launched a new report Procurement in the Finishes, Fit-Out and Interiors Sector, aiming to better understand how procurement practices are affecting the £10 billion fit-out industry and most importantly, how they can be improved.

FIS last year raised concerns that the push for modern methods of construction was being undermined by lack of focus on modern methods of procurement. To better understand the evolution of procurement practices, the organisation commissioned Professor Stuart Green of the University of Reading to explore procurement practices in the UK fit-out sector. FIS has a close working relationship with AMA Research, who were also keen to explore this topic and support this work and were able to offer assistance in developing the survey and extending the reach for participation.

This result is a fascinating new report that benchmarks current practices from those contractors directly involved and explores how procurement impacts effective delivery. Through better understanding of the challenges facing the industry, the sector can deliver better value and improve supply chain relationships.

The nature of the procurement process is often identified as a barrier to change. Dame Judith Hackitt’s statement from the 2018 ‘Building a Safer Future’ Report, confirmed that ‘Improving the procurement process will play a large part in setting the tone for any construction project. This is where the drive for quality and good outcomes, rather than lowest costs must start.’

FIS Chief Executive Iain Mcllwee stated:

“The key to unlocking the potential of construction and unleashing the culture change that we need in the finishes and interiors sector sits squarely in procurement. That isn’t a revelation. Virtually every report written about the construction process has raised concerns about procurement practices that facilitate a race to the bottom and create adversarial relationships and it crops up in almost every conversation I have about improving the sector. This is felt most acutely in our sector which absolutely sits at the whip end of construction when programmes and budgets are stretched or there is huge pressure to get the work done to leverage the value of a building.”

This new report furnishes the ongoing debate with concrete data and provides a voice to those who work in the fit-out sector. It is based on both a questionnaire conducted online during July and August 2022 that returned 269 responses with 100% quality rating on results and then supplemented with 20 in-depth interviews with selected practitioners representing contractors operating at all tiers of the supply chain. The research raised serious questions about time allocation in procurement and tendering processes, and worryingly how risks are routinely pushed down the supply chain.

Professor Stuart Green, School of Construction Management and Engineering at the University of Reading said:

“I have been hugely impressed with the leading-edge firms in the fit-out and interiors sector. They are crucially focused on delivering high-quality work to demanding deadlines. Such firms act as exemplars for collaborative working at its very best.

“But many firms within the sector don’t get the chance to work collaboratively. This is especially true of the smaller firms who act as subcontractors. Procurement practices are too often focused on low-cost tendering with little consideration of other factors. Subcontractors are further obliged to accept highly onerous conditions of contract which undermine trust from the outset. The smaller firms are frequently pressurised to reduce their tender price retrospectively and to offer discounts in return for prompt payment. It seems that old-fashioned subbie bashing is alive and well in the fit-out sector. This cannot be the basis upon which to sustain a modern industry.”

Laura Pardoe, Director at AMA Research said:

‘Connecting with people working directly in the field helps understand the real issues they are dealing with daily. This is critical to being able to decipher what needs improving. It has been a pleasure to support FIS in reaching out to people across their sector to canvass views and gather thoughts and experiences. The objective perspective we can bring as an expert researcher provides robustness to our understanding across the array of issues uncovered.’

In conclusion, Iain Mcllwee said:

“The regulatory, environmental, commercial and moral drivers for change have never been stronger and this research-based report has given a voice to all in the supply chain and is the start of a practical call to action for positive change.”

by Clair Mooney | 15 Feb, 2023 | Main News Feed

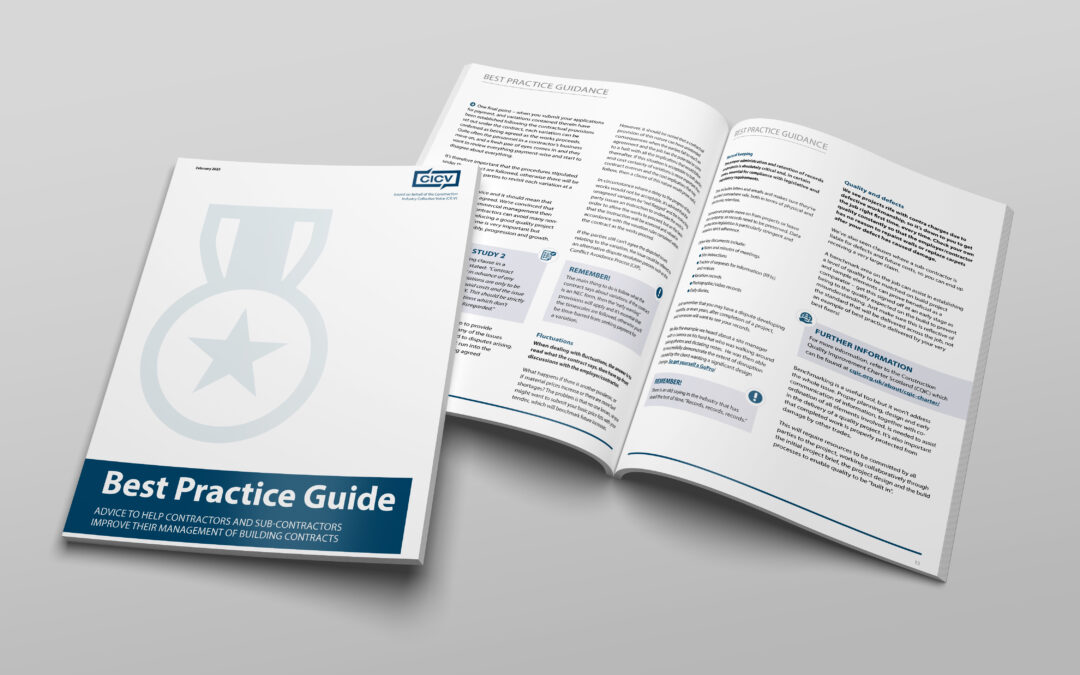

The Construction Industry Collective Voice (CICV) has followed up the results of its recent payments survey by issuing a new Best Practice Guide to help contractors and subcontractors improve cashflow and prevent costly and damaging disputes

Compiled by more than a dozen industry experts, the in-depth guide offers a wealth of practical information, demonstrating how to take control and proactively deal with a range of issues to enhance the entire contractual chain.

As part of its mission to improve the sector, the open source publication is being supported by an upcoming webinar on Friday 3 March that will see experts from the CICV talk through the guide and offer further insights into preventing financial disagreements.

Both resources have been produced in response to last week’s CICV survey on payment and cashflow issues in the industry in Scotland, which revealed that businesses are still suffering the scourge of late payments, outstanding retentions and unexpected charges.

Iain McIlwee, FIS Chief Executive said:

“It has been great to work colleagues from across the CICV to develop this guidance. It is vital that the supply chain becomes more contractually aware and fully understands the risks they are being asked to carry. This document is something every contractor should use to ensure that they and their teams are contractually aware and making good decisions. It is a great training tool too for those joining the sector. The CICV is an amazing force for good and we are very proud to be part of it.”

Industry consultant Len Bunton, who is Chair of the CICV Pipeline and Commercial sub-group, said:

“Following the recent CICV survey, we concluded that the contracting supply chain needed some guidance on improving the commercial management of projects.

“Our highly-experienced contributors have walked through the construction process, giving their best recommendations on how to do things better day-to-day. A lot of the problems we deal with are self-inflicted, so we have gone back to the basics of improving the way in which commercial activities are carried out.

“This is not rocket science, but it’s clear the whole process needs a massive shake-up. Following publication of the guide and our webinar to take the supply chain through it, I am confident we can get change into the UK industry.”

As the latest initiative from the respected industry body, the Best Practice Guide is free to download from the CICV website and looks at a number of areas of interest, including:

- Tender qualifications

- Contract amendments

- Payment schedules

- Payment applications

- Payments received and value

- Variations

- Retentions

- Fluctuations

- Notices

- Record keeping

- Quality/defects

- Conflict Avoidance Process (CAP).

The guide has been drawn up by experts from a range of industry bodies, including Mr Bunton, Finishes and Interiors Sector CEO Iain McIlwee, Scottish Building Federation Commercial Director Ian Honeyman and the National Hub Programme Director of Scottish Futures Trust, David MacDonald.

Mr Honeyman said:

“Agreeing a mutually beneficial and collaboratively agreed contract is the first, vital stage in any construction project, and an area in which can lead to costly and damaging disputes.

“The CICV has therefore looked at the most common reasons for payments being delayed and changed, and has prepared this guide to help companies and individuals understand how to avoid them.”

CICV Chair Alan Wilson, who is also Managing Director of electrical trade association SELECT, said:

“Being paid on time and receiving what you’re due in full is essential for the survival and growth of every business, so this guide and accompanying webinar will help contractors and sub-contractors improve the commercial management of building contracts.”

The Best Practice Guide and webinar are the latest in a string of practical and constructive initiatives launched by the CICV since its creation as the Construction Industry Coronavirus (CICV) Forum in March 2020.

Made up of 28 trade associations, professional services bodies and companies, it has maintained a steady supply of information and practical advice to the sector as well as carrying out surveys, producing animations and posters, hosting webinars and maintaining close dialogue with Scottish Government ministers.

The CICV Best Practice Guide can be downloaded here and you can register for the upcoming webinar here.

by Clair Mooney | 7 Feb, 2023 | Main News Feed

Construction businesses in Scotland are still suffering the scourge of late payments, outstanding retentions and unexpected charges, a new survey by the CICV has revealed.

Some 68% of respondents said their payment terms were altered negatively, with 60% claiming adjustments to payments were made with little or no explanation. And 69% of those surveyed said the time and cost of chasing outstanding moneys was their most significant problem when it came to payment.

The in-depth survey on cashflow and payments was undertaken to help an accurate picture of the current financial landscape in the Scottish construction industry.

Answered by those businesses which operate both as main and subcontractors in the public and private sectors, its key findings included:

- 52% reporting that they still have problems getting retentions paid

- 44% revealing that they had been hit with unexpected charges

- 40% disclosing that they “always or often” had payments reduced

- 30% saying payment delays have a “major impact” on their company.

Some 50% of respondents said they required external assistance to deal with payment disputes, with 54% saying they had referred a dispute to adjudication.

And 62% of those surveyed also said they were aware of project bank accounts, but only 17% had actually used them.

Len Bunton, Chair of the CICV’s Pipeline & Commercial sub-group, said:

“From these findings, it is clear – and also rather depressing – that cashflow and payment issues are still major problems in the construction industry in Scotland.

“It is especially frustrating to see so many financial disputed still going to costly adjudication and so little take-up of solutions like project bank accounts and the Conflict Avoidance Process – despite evidence that they do work and help to improve all-important cashflow.”

The survey also invited respondents to provide anecdotal evidence of cashflow and payment issues, along with suggestions of how to improve the current situation.

One said: “I’d like to see less subcontracting and more directly employed trades so there’s a joined-up process and effectively one large purse with collective ownership. The minute we sub-contract we divide, and priorities, focus and responsibility aren’t truly shared.”

Another told the poll: “We have problems with the public sector with too many authorisations that prolong and delay payment. A simplified process would help.”

A third added: “Many years ago, main contractors had to show proof of payment to sub-contractors before they received their next payment. Implementing such a practice for all sub-contractors would hugely improve the payment process.”

While a fourth respondent said simply: “Employers need to be held accountable and measured against the agreed payment terms within the building contract.”

The CICV is now devising a series of measures to help combat issues highlighted in the survey, including the imminent publication of a best practice guide. The collective is also planning an online webinar, offering contractors practical advice to help them avoid payment pitfalls.

David MacDonald, who is also a member of the CICV’s Pipeline & Commercial sub-group, added: “The many troubling issues highlighted by this survey simply reinforce the need for the industry to resolve matters before they escalate into disputes.

“The best practice guide, to be published by the CICV shortly, is designed to be used to eliminate poor commercial management and assist contractors to be much more alert to potential problems and risks.

“The planned webinar will also help contractors navigate the perilous waters of payment, which are clearly still littered with many difficulties.”

The survey is the latest in a string of practical and constructive initiatives launched by the CICV since its creation as the Construction Industry Coronavirus (CICV) Forum in March 2020.

Made up of 28 trade associations, professional services bodies and companies, it has maintained a steady supply of information and practical advice to the sector as well as carrying out surveys, producing animations and posters, hosting webinars and maintaining close dialogue with Scottish Government ministers.

- A full copy of the survey can be download here.