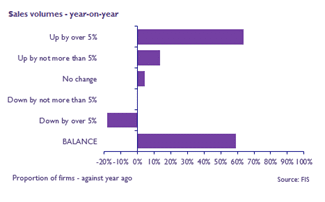

The FIS Latest Trends Survey indicates that overall 58% of respondents reported increased quarterly sales in Q2 2021. Looking into the next quarter, the market is even more optimistic than in Q1 with a balance of 70% expecting increased sales in Q3 and despite material and labour shortages a balance of 33% anticipating this will convert into increased volumes of work. Looking into 2022 81% of respondents are anticipating increases in sales to continue into 2022.

Shortages remain the biggest concern to market expansion with material shortages acute and labour shortages becoming ever more a concern. Over 60% of firms reporting labour shortages with 22% reporting that the availability of migrant workers has now fallen by more than 25%. The situation will not ease over the summer with holiday plans adding to the pressure – 71% of firms are anticipating problems over the next 12 months. Drylining, Ceiling, Fixing, Plastering, Carpentry and Joinery and Partitions Installer all being listed as areas of concern. Worryingly, whilst 48% believe the major issue is COVID delaying return, 34% predict that the labour will not return.

Commenting on the report, FIS CEO, Iain McIlwee stated: “The numbers reflect the conversations that we are having – there is work out there and members are getting busy. The conditions in the market, however, remain incredibly difficult and despite inflation, packages continue to be squeezed hard to hit unrealistic tender prices and programmes. It is imperative that, as a supply chain, we recognise the only way to ensure that shortages do not cause chaos is to plan better, build time into the procurement process and ensure that engagement is early enough to minimise design and programme problems that result in rework and waste. We also have to ensure commitment is given and contracts are exchanged earlier, ensuring that there is sufficient time to support the complex and precise planning, enabling labour and materials to be secured to deliver quality. The days of snapping your fingers on a Friday and 60 bodies arriving on site on Monday have to be consigned to the past.”

The FIS Q2 Market Trends Survey is available for download here

FIS works in collaboration with the Construction Products Association (CPA) to produce this report and manufacturing data is aggregated as part of their wider survey. The wider manufacturing sector posted a fourth successive quarterly expansion in the second quarter of 2021, according to the latest Construction Product Association’s (CPA) State of Trade Survey. Private housing, infrastructure and private housing repair, maintenance and improvement (rm&i), in which activity remains firmly above pre-coronavirus levels, continued to be the main drivers of growth. Material cost inflation, however, remained a prominent feature and supply-side constraints were seen as the key concern for the year ahead. The full CPA survey can be downloaded here.

Market Data

FIS has access to a wide range of market data from sources including the CPA, Barbour ABI and Builders’ Conference. In addition, FIIS produces a state of trade survey specifically for the finishes and interiors sector.