The UK economy continued its stronger than expected recovery in July, growing by 6.6% following June’s expansion of 8.7%. The economy has now recovered around half of the lost output between March and May, it remains 11.7% smaller than in February: to put it in context, the economy is the same size now that it was in 2013.

While the speed of the economy is encouraging, many experts’ current sentiments are very downbeat: this is because many indicators have weakened recently and are expected to deteriorate further. The UK currently faces a triple threat of:

- a weakening economic outlook set to deteriorate further as emergency government support measures are withdrawn later in the autumn,

- new Covid-19 outbreaks leading to restrictions that inhibit further economic recovery, and

- a disruptive Brexit causing shortages of goods and labour, and price inflation among other disruptions.

The Bank of England’s Chief Economist recently warned the government against extending the furlough scheme, arguing it would delay a “necessary process of adjustment” and the focus should be on transitioning to new ways of working.

Sector comparison

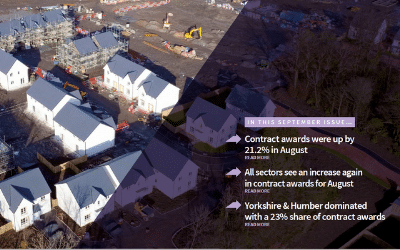

Construction continued its strong recovery, growing by a further 18% in July after being the most impacted sector in April. Further detail is contained within the report.

The production sector output increased by 6%, led by the manufacture of clothes and transport equipment. Services also increased by 6% with wholesale and retail trade, information and communication and defence approaching recovery to February’s levels. Accommodation and food services, while growing strongly, is still 40% compared to earlier in the year.

Construction remains 25% down compared to February, with services -13% and manufacturing -12%.